Add your feed to SetSticker.com! Promote your sites and attract more customers. It costs only 100 EUROS per YEAR.

Pleasant surprises on every page! Discover new articles, displayed randomly throughout the site. Interesting content, always a click away

Berger Financial Group

Investing in YouWhy Market Downturns Are a Gift for Wealth Builders 14 Apr 2025, 4:19 pm

In Q1 2025, the market took another dip, inching us closer to bear market territory after years of impressive gains. For many, this felt like a cause for concern—but for those in the accumulation phase of financial planning, it’s actually a golden opportunity. If you’re building wealth for the future, here’s why you should see market downturns as a chance to supercharge your portfolio rather than something to fear.

A Sale on Your Favorite Investments

When the market drops, stock prices fall. That means you can buy more shares with the same amount of money. Imagine walking into a store and finding your favorite items on sale—except this time, it’s your investments. If you’re contributing regularly, whether through a 401(k), IRA, or monthly investments, a lower market stretches your dollars further. Each contribution buys you more ownership in the companies or funds you believe in. Over time, as the market recovers—and history shows it always has—those extra shares can translate into significant growth.

The Power of Staying the Course

This is where dollar-cost averaging shines. By investing a fixed amount consistently, regardless of market conditions, you’re not trying to time the highs and lows. Instead, you’re taking advantage of them. When prices are low, you scoop up more shares; when they’re high, you buy fewer. Over the long haul, this strategy smooths out volatility and sets you up for bigger gains. The trick? Discipline. It’s tempting to pause or pull back when headlines scream about downturns, but sticking to your plan is what turns these dips into wins.

Turning Fear Into Opportunity

Market downturns don’t last forever. They’re a natural part of the economic cycle, and every bear market in history has been followed by a recovery. For those in the accumulation phase, this isn’t a setback—it’s a chance to accelerate your wealth-building journey. The shares you buy at a discount today could be the foundation of your financial security tomorrow.

So, the next time the market takes a tumble, don’t panic. See it for what it is: a rare opportunity to invest in your future at a bargain. Keep your eyes on the long game, stay disciplined, and let these downturns work in your favor.

Asset Allocation by Age: What You Need to Know at Every Life Stage 9 Apr 2025, 1:00 pm

The way you invest changes with time. Your financial priorities in your 20s will look very different from those in your 60s, and so should your investment strategy. Asset allocation—how you divide your investments across stocks, bonds, and other assets—is one of the most critical factors in building a successful financial plan.

Let’s explore how your allocation should evolve with age to help you grow your wealth, manage risk, and secure a comfortable retirement.

Why Asset Allocation Matters

Asset allocation isn’t a one-size-fits-all strategy. Different types of investments carry varying levels of risk and return, and your personal tolerance for risk changes over time. Equities, such as individual stocks, often deliver higher returns but come with more volatility. Bonds, on the other hand, are generally considered safer but offer lower returns. Striking the right balance between these and other asset classes is essential to optimize growth while protecting your portfolio.

Asset Allocation by Age

Your asset allocation strategy should evolve as you progress through different stages of life. Here’s a breakdown of how to think about your portfolio at each phase:

Early Career (20s and 30s): Building for Growth

When you’re young and just starting your career, time is your greatest ally. With decades ahead to recover from market downturns, you can afford to take on more risk. A portfolio in this stage might be 80% to 100% in equities. This aggressive approach allows you to capitalize on the long-term growth potential of stocks. Equities historically outperform other asset classes over the long run, helping you maximize returns while spreading risk.

Mid-Career (40s and 50s): Balancing Growth and Stability

As you advance in your career, your financial responsibilities likely increase. You may have a mortgage, children’s education to fund, and retirement savings to grow. While growth remains important, stability starts to take precedence. A balanced portfolio might include 60% to 80% in equities and 20% to 40% in bonds. Bonds provide stability and help reduce the impact of stock market volatility.

Pre-Retirement (60s): Protecting What You’ve Built

As you approach retirement, the focus shifts to preserving the wealth you’ve accumulated. With less time to recover from market downturns, reducing risk becomes essential. Many experts suggest a 50/50 split between equities and bonds or even a 40/60 mix. While equities still offer growth potential, bonds provide a safety net, ensuring you have the funds you need when you retire.

Retirement: Prioritizing Income and Preservation

Once you’ve retired, often your investment portfolio’s primary purpose is to provide steady income and ensure your savings last. Portfolios in retirement often skew heavily toward bonds, with 70% to 100% allocated to fixed-income investments. Fixed-income assets provide predictable returns and help shield your portfolio from market fluctuations.

Key Considerations

Risk tolerance, time horizon, and regular rebalancing are critical factors to keep in mind when designing your asset allocation strategy. Periodically revisiting your portfolio ensures it aligns with your goals and adjusts as market conditions change.

Final Thoughts

Asset allocation by age is a cornerstone of effective portfolio management. By adjusting your strategy at every life stage, you can maximize growth during your early years, balance risk in mid-life, and preserve capital as you near retirement. Contact Berger Financial Group today to ensure your investments align with your goals and life stage.

Is it Better to Pay Off Debt or Invest Your Extra Cash? 2 Apr 2025, 1:00 pm

Many people find themselves at a crossroads when deciding what to do with extra cash: should they pay off debt or invest? This is not a one-size-fits-all question. Your financial situation, goals, and the kind of debt you hold all play a key role in this decision. Whether you’re looking to get rid of debt quickly or grow your wealth over time, understanding the pros and cons of each approach can help you make an informed choice.

Understanding the Interest Rate Factor

When deciding whether to pay off debt or invest your extra cash, the first factor to consider is the interest rate on your debt. Not all debt is created equal, and the type of debt you have will greatly influence your decision.

High-Interest Debt

If you have high-interest debt, such as credit card balances or payday loans, it almost always makes sense to pay it off first. The reason is simple: the interest on these debts can quickly outweigh the returns you would earn from most investments. For example, credit card interest rates can range anywhere from 15% to 30%. It’s unlikely you’ll find an investment with a guaranteed return that high. By paying off high-interest debt, you are essentially earning a risk-free return equal to the interest rate.

Low-Interest Debt

On the other hand, low-interest debts like mortgages or student loans can be approached differently. These debts typically come with interest rates well below the long-term average return of investments like stocks. For instance, if your mortgage has a 3% interest rate and the stock market’s historical average return is 7%-8%, it may make more sense to invest your extra cash rather than pay off the debt early. By investing, you could earn a higher return on your money over time.

Choosing a Strategy for Paying Down Debt

If paying off debt is your priority, it’s important to choose the right strategy to manage your payments effectively. Two popular methods are the Debt Snowball Method and the Debt Avalanche Method. Each has its own advantages depending on your personality and financial goals.

The Debt Snowball Method

The debt snowball method focuses on building momentum to keep you motivated. Here’s how it works:

- List all your debts in order from smallest to largest balance.

- Make minimum payments on all debts except the smallest one.

- Allocate all extra cash toward paying off the smallest balance.

- Once that debt is eliminated, move on to the next smallest balance, and repeat.

This method is designed to provide emotional wins by quickly eliminating smaller debts, which can keep you motivated to stick to your repayment plan.

The Debt Avalanche Method

The debt avalanche method, on the other hand, is all about saving money on interest. The steps are as follows:

- List all your debts in order from highest to lowest interest rate.

- Make minimum payments on all debts except the one with the highest interest rate.

- Allocate all extra cash to the debt with the highest interest rate.

- Once that debt is paid off, move on to the next highest interest rate, and repeat.

This method will save you the most money over time because you’re tackling the most expensive debt first.

Balancing Debt Repayment and Investing

For many people, the best solution lies somewhere in the middle. You don’t always have to choose between paying off debt or investing your extra cash—you can do both. For example:

- Allocate some of your extra cash toward high-interest debt to eliminate it quickly.

- Use the remaining portion to invest in opportunities with strong growth potential.

This balanced approach allows you to reduce your debt while still taking advantage of the power of compound interest to grow your wealth.

What’s Right for You?

High-interest debt should almost always be tackled first, as it drains your finances faster than most investments can grow. For low-interest debt, investing may be the better choice, especially if your returns are expected to exceed the debt’s interest rate.

No matter what you decide, having a clear plan will help you achieve financial independence. Contact Berger Financial Group today to get personalized advice tailored to your needs.

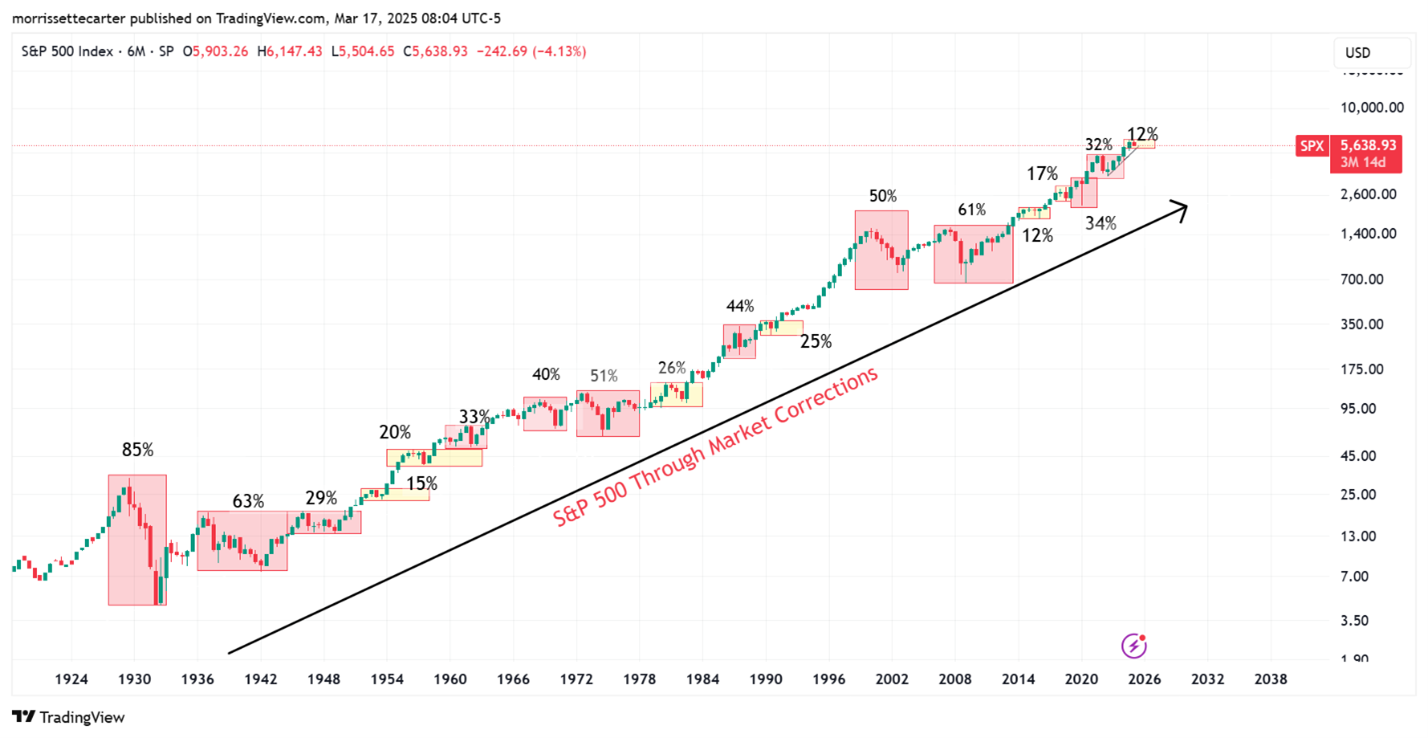

Stock Market Pullbacks: What They Are and How Often They Happen 25 Mar 2025, 3:15 pm

If you’ve ever watched the stock market dip and wondered, “Is this normal?”—the answer is yes! Stock market pullbacks, those moments when prices drop from their recent highs, are a regular part of investing. They can feel scary, but history shows they happen all the time. Let’s break down what pullbacks look like and how often they’ve shown up over the last 100 years, based on the S&P 500, a key measure of U.S. stocks.

What’s a Pullback?

A pullback is just a fancy way of saying the stock market takes a step back. Imagine prices climbing a hill, then sliding down a bit before (often) heading back up. We measure pullbacks by how much the market falls from its peak—say, 5%, 10%, 15%, or 20%. Each size tells us something different about what’s going on.

The Small Dip: 5% Pullbacks

A 5% drop is like a speed bump—small and super common. Over the past 100 years, the stock market has hit a 5% dip in about 94 out of every 100 years. That’s almost every single year! Sometimes it happens a few times in one year, like little hiccups. It’s so normal that investors barely blink at it—it’s just the market taking a quick breather.

The Correction: 10% Pullbacks

When the market falls 10%, we call it a “correction.” It’s a bigger dip, like stepping into a shallow puddle. History shows this happens in about 6 out of every 10 years—roughly once every year and a half or so. It’s noticeable, but it’s still pretty routine. Think of it as the market saying, “Whoa, let’s slow down a bit.”

The Deeper Drop: 15% Pullbacks

A 15% decline feels more serious, like sliding halfway down a playground slide. Over the last century, this has happened in about 4 out of every 10 years—around once every 2.5 years. It’s not as common as the smaller dips, but it’s still something investors see fairly often. It might signal tougher times, but it’s not a full-on crisis.

The Big One: 20% Pullbacks

When the market drops 20% or more, we enter “bear market” territory. It’s like tumbling all the way down that slide! This has happened in about 1 out of every 4 years over the past 100 years. These are the big drops that grab headlines, often tied to economic slowdowns or surprises. But here’s the thing: not every 20% drop turns into a long disaster—sometimes the market bounces back by year’s end.

Despite numerous double digit drops, the S&P 500 is up over 19,000% total return going back to the 1920’s

Investors in the S&P 500 over the last decade were handsomely rewarded, but this timeframe also included multiple “painful” pullbacks. They were painful in the moment, but when you zoom out just a little bit, you realize they are part of the price we pay for good long-term returns

Why This Matters

Pullbacks sound bad, but they’re just part of how the stock market works. Over time, it tends to climb higher, even with these dips along the way. Think of it like a hike: there are downhill stretches, but the trail still leads up the mountain. For example:

- A 5% dip? Expect it almost every year.

- A 10% correction? About once every year and a half.

- A 15% drop? Roughly once every 2.5 years.

- A 20% bear market? Around once every 4 years on average.

The Bright Side

These drops can actually be opportunities. When prices fall, it’s like stocks going on sale—great for people who want to buy in and hold on for the long haul. The last 100 years show that after pullbacks, the market often recovers and keeps growing. Sure, big drops like the Great Depression or 2008 stick in our minds, but smaller dips happen way more often and don’t last forever.

Takeaway

Stock market pullbacks are normal, not a sign the sky is falling. Whether it’s a tiny 5% dip or a bigger 20% plunge, they’ve been happening for a century and will keep happening. Knowing how often they pop up—based on this 100-year track record—can help you stay calm and smart about investing. So next time the market wobbles, just remember: it’s probably been here before, and it’ll likely climb back up again.

Married Filing Jointly vs. Separately: Which Is Better? 19 Mar 2025, 1:00 pm

Your tax filing status can significantly affect how much you owe or receive during tax season. For married couples, choosing between filing jointly or separately is an important decision that depends on your financial situation. Both options have advantages and drawbacks, from tax bracket differences to eligibility for certain deductions and credits. Understanding how each status works and the benefits they provide can help you maximize savings and avoid unnecessary tax burdens.

Understanding the Basics of Filing Jointly vs. Separately

When you’re married, the IRS allows you two primary filing options: Married Filing Jointly or Married Filing Separately. Both options come with their own rules, tax brackets, and implications for deductions and credits.

Married Filing Jointly

When you choose to file jointly, you and your spouse combine your income on one tax return. This often provides significant benefits, including access to wider tax brackets and valuable credits.

Joint filers can take advantage of:

- Lower overall tax rates due to wider brackets

- Access to key tax credits like the Earned Income Tax Credit

- (EITC), Child Tax Credit, and American Opportunity Credit Higher deduction thresholds for certain expenses, such as medical costs

For most couples, filing jointly typically leads to a lower overall tax bill. Combining your incomes into one return can push more of your earnings into lower tax brackets, effectively reducing the taxes owed.

Married Filing Separately

On the other hand, Married Filing Separately means each spouse files their own individual return, reporting their income, deductions, and credits separately. While this option is less common, there are circumstances where it may be beneficial.

Separate filing can be advantageous if:

- One spouse has significant medical expenses

- One partner has legal or financial issues, such as unpaid taxes, defaulted loans, or bankruptcy

- You want to protect yourself from a spouse’s potential tax liability

However, this filing status comes with several drawbacks, including narrower tax brackets, which may result in higher taxes for each spouse.

Tax Brackets: How Filing Status Impacts What You Pay

One of the most significant differences between filing jointly and separately lies in the tax brackets.

- Married filing jointly provides access to wider tax brackets, allowing couples to combine their income and potentially pay less tax overall. For example, if one spouse earns significantly more than the other, their combined income can be taxed at a lower rate when filing jointly.

- Married filing separately comes with narrower tax brackets, meaning each spouse’s income is taxed individually at higher rates. This can often result in a higher combined tax bill compared to filing jointly.

Example of Tax Bracket Impact

Let’s say Spouse A earns $80,000, and Spouse B earns $20,000. Filing jointly allows the couple to combine their income ($100,000) and benefit from a lower overall tax rate. If they file separately, Spouse A’s income might push them into a higher tax bracket, increasing the tax owed.

The Impact on Deductions and Tax Credits

When deciding whether to file jointly or separately, it’s essential to consider how your filing status affects deductions and credits. Married Filing Jointly provides greater access to valuable tax benefits, while filing separately can limit or eliminate these opportunities.

Credits and Deductions Available to Joint Filers

Certain tax credits and deductions are only available or more generous to those who file jointly:

- Earned income tax credit (EITC): Not available to couples filing separately

- Child tax credit: Reduced or eliminated for separate filers

- Education credits: The American Opportunity Credit and Lifetime Learning Credit are often unavailable for those filing separately

Medical Expenses: An Exception to the Rule

While Married Filing Jointly typically offers the most benefits, there are exceptions. Filing separately can be a smart choice if one spouse has significant medical expenses.

Medical expenses are deductible only if they exceed 7.5% of your adjusted gross income (AGI). By filing separately, the spouse with high medical costs can use their individual, lower AGI to qualify for a larger deduction.

When Filing Separately Makes Sense

While most couples benefit from filing jointly, there are scenarios where filing separately may be the better option:

- High medical expenses: As mentioned, filing separately can help deduct large medical costs.

- Legal or financial issues: If one spouse has unpaid taxes, defaulted loans, or other financial problems, filing separately can protect the other spouse from liability.

- Income-based repayment for student loans: Filing separately can sometimes lower payments for income-driven repayment plans, as only the individual’s income is considered.

If any of these situations apply to you, it’s worth considering the separate filing option.

Can You Switch Between Filing Statuses?

The good news is that your filing status isn’t permanent. If you choose to file separately one year, you can switch to Married Filing Jointly the next, as long as you meet the qualifications. This flexibility allows couples to adapt their filing status to their changing financial circumstances.

Which Filing Status Is Better for You?

So, which is better: married filing jointly or separately? Ultimately, the right choice depends on your financial situation. For most couples, filing jointly provides the greatest tax savings through wider brackets, access to credits, and lower overall rates. However, for couples with unique circumstances—such as high medical costs or financial liabilities—filing separately can offer better protection or savings.

Steps to Make the Right Choice

- Run the numbers both ways: Calculate your taxes using both filing statuses to see which provides the most benefits.

- Consider your eligibility for credits and deductions: Evaluate how each option impacts your access to credits like the EITC or Child Tax Credit.

- Consult a tax professional: A tax advisor can help you determine the best filing status based on your unique situation.

Conclusion

Deciding between Married Filing Jointly and Married Filing Separately isn’t a one-size-fits-all answer. While joint filing typically provides greater financial benefits for most couples, there are situations where separate filing makes sense. By understanding the rules, evaluating your eligibility for key tax credits, and calculating your potential outcomes, you can make the right decision for your family. Contact Berger Financial Group today.

Annuity vs. IRA: What’s the Difference? 12 Mar 2025, 1:00 pm

Planning for retirement requires making key financial decisions. Two of the most commonly used tools are annuities and Individual Retirement Accounts (IRAs). While both offer tax advantages and help you prepare for the future, they differ in structure, flexibility, and benefits. Knowing how these options work and their key differences can help you choose the one that best aligns with your retirement goals.

Let’s take a closer look at what annuities and IRAs offer and how to decide which option is right for you.

What Are Annuities and IRAs?

Before we dive into the key differences, it’s essential to define what annuities and IRAs are:

- An annuity is a financial product sold by insurance companies that provides a stream of income, often for life. You can purchase it in a lump sum or through regular payments, and it’s designed to ensure steady income during retirement.

- An IRA, on the other hand, is a tax-advantaged investment account that individuals can use to save for retirement. It comes in two primary forms: Traditional and Roth.

Both options have a shared goal—helping you save for retirement—but they operate in distinct ways.

Key Differences Between Annuities and IRAs

1. Tax Treatment

Both annuities and IRAs provide tax-deferred growth, meaning your investments can grow without being taxed each year. However, the taxation rules for withdrawals differ:

- Traditional IRAs: Withdrawals are taxed as ordinary income. Contributions are typically tax-deductible, providing an upfront tax benefit.

- Roth IRAs: Contributions are made with after-tax dollars, but qualified withdrawals are entirely tax-free.

- Annuities: Earnings are taxed as ordinary income upon withdrawal, similar to Traditional IRAs. Unlike IRAs, contributions to annuities are not tax-deductible.

This distinction matters when planning for your taxable income during retirement.

2. Contribution Limits

Another significant difference between annuities and IRAs is how much you can contribute each year.

- IRAs: For 2024, the contribution limit is $6,500 (or $7,500 for those aged 50 and older).

- Annuities: There are no contribution limits, allowing you to invest as much as you’d like.

If you have already maxed out your IRA contributions and want to save more, annuities may provide additional flexibility.

3. Withdrawal Rules and Penalties

Accessing your funds also varies significantly between these two options.

- IRAs: Penalty-free withdrawals are allowed after age 59½. Early withdrawals before this age incur a 10% penalty plus income taxes (with some exceptions). For Roth IRAs, contributions (but not earnings) can be withdrawn anytime without penalty.

- Annuities: Withdrawals before age 59½ also incur a 10% penalty. Additionally, many annuities have a surrender period during which withdrawals are subject to extra fees. Once the surrender period ends, withdrawals are treated as taxable income.

Understanding these rules is crucial to avoid unexpected penalties and ensure you can access your funds when needed.

4. IRA to Annuity Rollovers

It’s possible to roll over funds from an IRA into an annuity, but this must be done carefully to avoid unnecessary taxes or penalties. A direct, tax-free rollover is an option, but you should evaluate whether the annuity aligns with your financial goals and retirement timeline. Keep in mind that some annuities may impose surrender charges, especially if accessed early.

5. Investment Options and Flexibility

The level of control you have over your investments is another major factor:

- IRAs: These accounts offer broad investment flexibility, including options like stocks, bonds, ETFs, and mutual funds. This allows you to customize your portfolio to match your risk tolerance and goals.

- Annuities: Investment options are more limited and often focus on fixed, variable, or indexed returns. Annuities prioritize guaranteed income over growth potential, making them less flexible for those looking to diversify heavily.

While annuities provide security, IRAs offer more room for growth and adaptability.

Which Option Is Right for You?

Choosing between an annuity and an IRA depends on your unique financial situation and retirement objectives. Here are some factors to consider:

- Guaranteed Income Needs: If you prioritize a steady, predictable income in retirement, an annuity may be the better choice.

- Flexibility: If you want more control over your investments or prefer tax-free withdrawals in retirement, a Roth IRA might be a better fit.

- Savings Goals: If you’ve maxed out IRA contributions but still want to invest more, annuities can supplement your savings.

Ultimately, the decision should reflect your risk tolerance, financial goals, and the level of security you need for your retirement.

Final Thoughts

Understanding the differences between annuities and IRAs is essential for building a robust retirement strategy. While both options offer tax advantages and opportunities for growth, their rules, limits, and benefits vary widely. By knowing how each works, you can choose the one—or a combination of both—that best supports your long-term financial goals.

Always consult with a financial advisor before making any significant decisions. They can help you navigate these options and create a plan tailored to your needs. Contact Berger Financial Group today to start planning your secure and successful retirement!